However careful the practitioner, errors creep into submitted returns: a transposed digit, a missing employee, a wrong currency split, a withholding-tax line forgotten. The Amend workflow on Submitted Returns is TaRMS’s acknowledgement that returns are not infallible. This lesson teaches when and how to use it.

TaRMS Essentials Lesson 4.3

Amending Current-Period Submitted Returns

Submit-then-realise-it-is-wrong is the most common return-filing experience. The Amend workflow on Submitted Returns is the clean route to correction without recourse to the formal objection process.

1

Executive summary

When amendment is permitted under TaRMS practice and the relationship to the section 62 ITA objection regime.

2

Lesson content

The Amend workflow click-by-click, with consequences for the assessment, ledger, and Single Account.

3

Assessment & policy notes

When to amend vs. when to object, and how to keep the audit trail clean.

A. Lesson Context: Errors are Inevitable

B. Legislative Framework

1. Section 41 ITA — assessment on basis of return

The Commissioner assesses on the basis of the return submitted. Amending the return resets the assessment to reflect the corrected figures.

2. Section 62 ITA — objection

The 30-day objection window is the formal route to dispute an assessment. Amendment within the same period is administratively cheaper and does not consume the objection window.

3. Practice Note on Amendments

ZIMRA permits amendment of a submitted return up to a defined period (typically up to the next return cycle, or until the assessment is finalised, whichever is earlier).

4. Interest and penalty implications

If amendment increases liability, interest accrues from the original due date (not the amendment date). Penalty may be waived if the amendment is voluntary and timely.

C. Detailed Conceptual Explanation

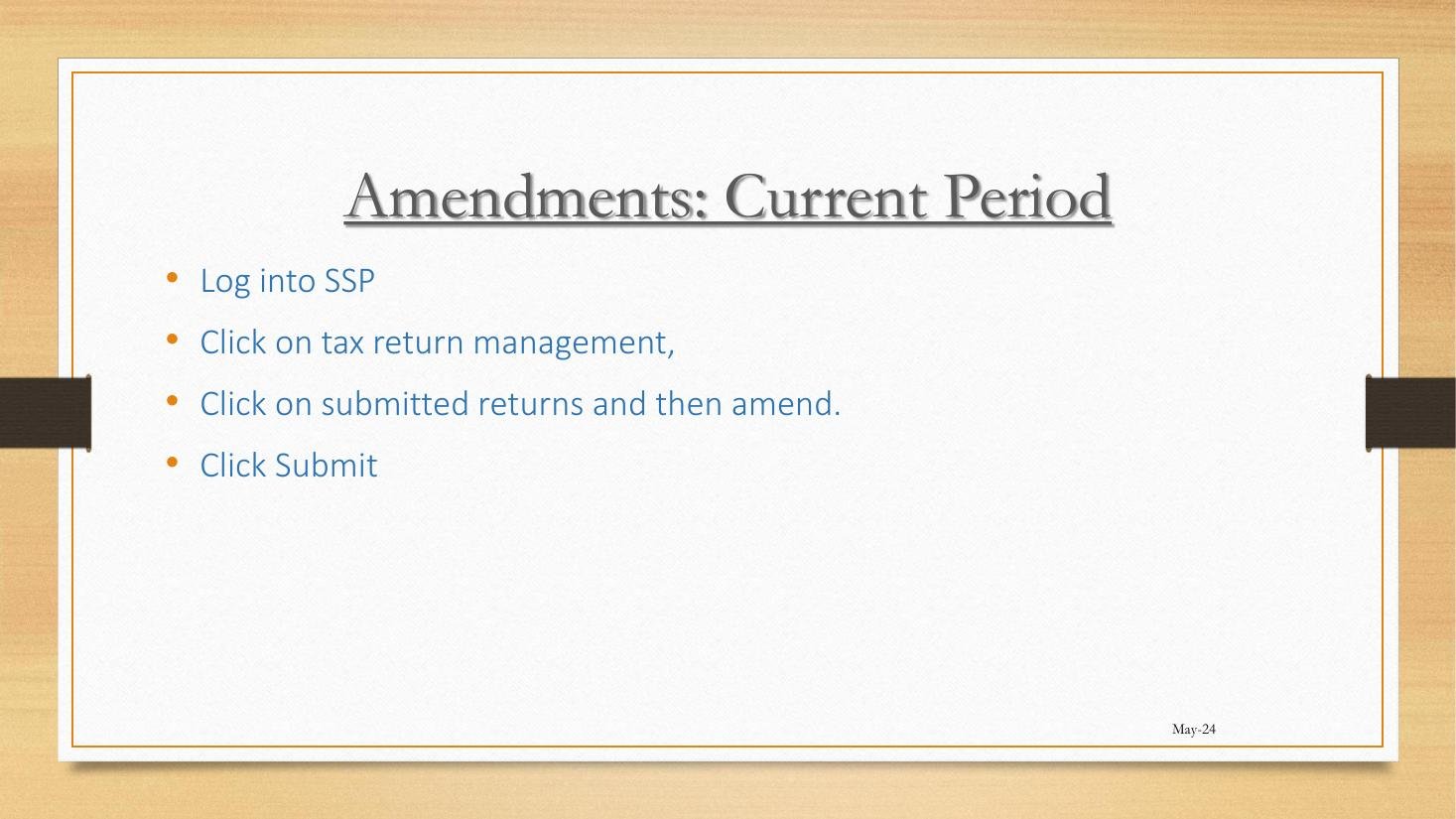

1. The four-step workflow

- Login to SSP → Tax Return Management.

- Click Submitted Returns.

- Locate the return; click Amend.

- Edit the data; click Submit. The amendment is acknowledged with a new reference; the assessment is reposted.

2. When amendment is allowed

| Trigger | Permitted? |

|---|---|

| Within the same return cycle, before next return is filed | Yes — routine. |

| Assessment notice issued, within 30 days, no formal objection lodged | Yes, with notification on the system. |

| Beyond 30 days, no objection lodged | Use the Voluntary Disclosure mechanism (VDA01) or section 47 reach-back via objection. |

| Audit in progress on the period | Generally not via Amend; coordinate with ZIMRA officer. |

3. The audit trail

Every amendment is recorded in the History tab of the relevant return. The original submission, all interim amendments, and the final amendment are visible in chronological order.

4. Interest and penalty mechanics

If the amendment increases liability:

- Additional liability dates back to the original due date.

- Interest accrues from the original due date at the prescribed rate.

- Penalty is in ZIMRA’s discretion; voluntary timely amendment usually attracts no penalty.

If the amendment decreases liability:

- The Single Account credit increases.

- A refund may be claimable.

- Where the original payment was made, no interest is due to ZIMRA.

5. Amend vs. Object — the decision matrix

| Situation | Recommended route |

|---|---|

| Clear arithmetic or data-entry error | Amend — faster, cheaper. |

| Disagreement with ZIMRA on legal interpretation | Object under section 62 ITA. |

| Mixed: some errors, some interpretation issues | Amend the errors; object the interpretation. |

| Period under audit | Coordinate with audit officer; do not amend unilaterally. |

D. Real-World Applicability

1. The missing-employee fix

Recall the question from Lesson 4.2: an employee was omitted from the PAYE return. Workflow: Submitted Returns → locate the PAYE return → Amend → add the employee row → resubmit. Additional liability is paid same-day via Single Account; interest accrues from the original due date.

2. The wrong-currency fix

An employer selected USD only when one employee was paid in dual currencies. Amend, switch to dual-currency selection, redo the template, resubmit.

3. The decreased-liability case

A practitioner discovers an over-claimed input VAT was included in the original return. Amend reduces the liability; the resulting credit sits on the Single Account or can be refunded.

4. The amendment-day playbook

- Identify the original return and the specific data field in error.

- Compute the correct figure and the impact on liability.

- Document the reason for the amendment (internal memo).

- Lodge the amendment via Submitted Returns → Amend.

- Pay any additional liability via Single Account same day.

- Confirm the Tax Type Report reflects the corrected assessment.

- File internal documentation in firm repository.

E. Case Law Integration

1. Re Eastview Suppliers (revisited) — voluntary timely amendment

A taxpayer who voluntarily amends and pays additional liability before audit selection is treated favourably under ZIMRA practice; penalty waiver is the norm.

2. Commissioner-General v. Marowa Holdings (Special Court 2023)

A taxpayer attempted to amend an old return after audit had commenced. The court held that the Amend workflow is not available once audit selection is communicated; the proper route is engagement with the audit officer, with formal disclosure documented.

3. The objection-vs-amendment choice

Section 62 ITA is the objection route. Amendment is an administrative correction. The two are distinct — objection requires legal articulation of disagreement; amendment is simple data correction. Mixing them creates procedural confusion.

F. Common Pitfalls

1. Amending during audit

Marowa Holdings (2023). Coordinate with ZIMRA officer.

2. Treating amendment as a form of objection

Section 62 ITA matters require formal objection. Fix: use the right tool.

3. Multiple sequential amendments

Looks like manipulation; ZIMRA may flag. Fix: get the amendment right the first time.

4. Forgetting the interest impact

Interest accrues from original due date. Fix: compute and pay total liability including interest.

5. Not documenting the reason

An audit later asks “why was this amended?” Fix: contemporaneous internal memo for every amendment.

G. Knowledge Check

Question 1

Walk through the four-step Amend workflow.

Question 2

When is amendment allowed and when is it not?

Question 3 — Scenario

You omitted an employee from the March PAYE return. The April return is not yet due. What do you do?

Question 4 — Scenario

You disagree with ZIMRA’s interpretation of an exemption applied in your March VAT return. Should you Amend or Object?

Question 5

What does Marowa Holdings (2023) say about amendment during audit?

H. Quiz Answers with Explanations

Answer 1

Tax Return Management → Submitted Returns → Amend → Submit.

Answer 2

Allowed within the same return cycle before next return; allowed within 30 days of assessment if no objection lodged. Not allowed during audit (coordinate with officer instead) and not the appropriate route for legal-interpretation disagreements (use objection).

Answer 3

Use the Amend workflow now: Submitted Returns → March PAYE → Amend → add the employee row → resubmit. Pay additional liability via Single Account; interest accrues from 10 April (the original due date for March PAYE). Internal memo records the reason.

Answer 4

Object. The disagreement is on legal interpretation, not on data. Lodge a formal objection under section 62 ITA within 30 days of the assessment. Amendment is wrong because it does not formally raise the legal issue.

Answer 5

The Amend workflow is not available once audit selection is communicated. The proper route during audit is engagement with the audit officer, with formal disclosure recorded in writing.

I. Key Takeaways

- Amend = data correction; Object = legal disagreement.

- Workflow: Submitted Returns → Amend → resubmit.

- History tab logs every amendment chronologically.

- Interest accrues from original due date on increased liability.

- Voluntary timely amendment usually attracts no penalty (ZIMRA practice).

- Do not amend during audit (Marowa Holdings 2023).

- Continuity: Lesson 4.4 covers back-filing of past missing returns.