Manual clearance is the route when automatic is unavailable but a certificate is genuinely needed for a specific business purpose. Common cases: an SME with one outstanding payment plan in progress; a taxpayer in current-period objection but not in default; a special clearance for a tender where the validity dates need to span specific months.

TaRMS Essentials Lesson 5.2

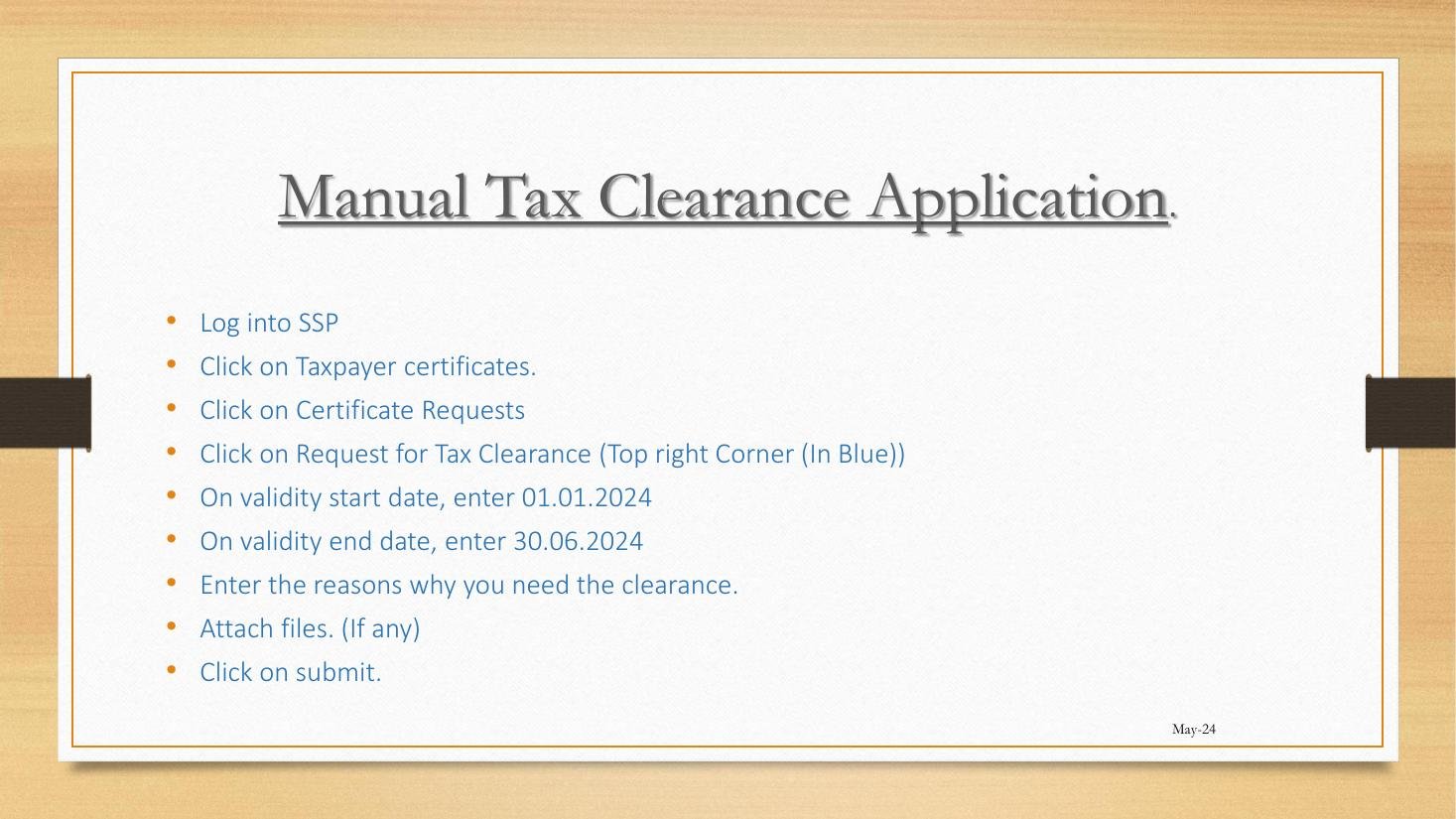

Manual Tax Clearance Application

When automatic clearance is unavailable but a clearance is genuinely needed, the manual application route lets the taxpayer state validity dates, articulate reasons, and attach supporting documents.

1

Executive summary

When manual clearance is appropriate vs. automatic, and the validity-window mechanism.

2

Lesson content

The Request for Tax Clearance (manual) workflow with field-by-field guidance.

3

Assessment & policy notes

Drafting tips for the “reason” field, attachment expectations, and post-submission follow-up.

A. Lesson Context: When Automatic Won’t Work

B. Legislative Framework

1. Section 80B ITA — the discretionary clearance

The Commissioner may issue clearance even where automatic eligibility is not met, on consideration of the taxpayer’s circumstances and the bona fides of the application.

2. Practice Note on Manual Clearance

ZIMRA Public Notice 2 of 2024 sets out the standard categories for manual clearance: payment-plan-in-place, current-period-objection-not-in-default, single-purpose tender, and miscellaneous Commissioner-discretion cases.

3. Validity dates

The taxpayer specifies start and end dates. ZIMRA may approve, vary, or reject. Practical maximum: 12 months.

4. Tender-specific clearance

For a single-tender purpose, validity matching the tender period is common.

C. Detailed Conceptual Explanation

1. Nine-step workflow

- Login to SSP.

- Click Taxpayer Certificates.

- Click Certificate Requests.

- Click Request for Tax Clearance (top-right blue button).

- Validity start date: enter the desired start (e.g., 01.01.2026).

- Validity end date: enter the desired end (e.g., 30.06.2026).

- Reason: enter the reasons why clearance is needed.

- Attach supporting files (tender documents, payment-plan acknowledgement, etc.).

- Click Submit.

2. Drafting the “reason” field

Three elements:

- The business purpose: e.g., “Bid for Tender XYZ-2026 issued by the Ministry of Energy, closing 15 June 2026.”

- The current compliance position: e.g., “All returns filed up to May 2026; April 2026 PAYE has a payment plan in place per ZIMRA Reference No. PP-1234.”

- The bona fides: e.g., “Granting clearance for the period 01 June – 30 September 2026 will allow Cairns Foods to participate in the tender; the payment plan continues to be honoured per schedule.”

3. Attachments expected

- Tender invitation document or supplier-onboarding form.

- Payment-plan acknowledgement (if applicable).

- Letter of intent from counterparty (if applicable).

- Latest Tax Type Report (downloaded from Lesson 7.2).

4. ZIMRA processing

Manual clearances are reviewed by an officer; turnaround typically 5–10 working days. Officer may request further clarification via Notifications.

5. Outcomes

| Outcome | Action |

|---|---|

| Approved with requested validity | Download certificate. |

| Approved with reduced validity | Use within reduced window; reapply if needed. |

| Conditional approval (e.g., subject to payment by date) | Meet condition; re-confirm certificate issuance. |

| Rejected | Read reasons; remediate or escalate. |

D. Real-World Applicability

1. Tender clearance

Cairns Foods bids on a tender closing in June. They request manual clearance with validity 01 June–30 September. ZIMRA approves; certificate downloaded and submitted with bid.

2. Payment-plan-in-place case

An SME has a 6-month payment plan on outstanding VAT. They need clearance for a supplier-onboarding. Manual application explaining the plan; ZIMRA grants 6-month validity matching the plan.

3. The objection-in-progress case

A trader has a section 62 objection pending on a single VAT assessment. All other heads are current. Manual application with reason “objection pending; not in default on any other head”; ZIMRA typically grants subject to the objection being prosecuted in good faith.

4. The application playbook

- Identify the business purpose and the validity dates needed.

- Audit current compliance position (Tax Type Report).

- Assemble attachments.

- Draft the “reason” per the three-element formula.

- Lodge via SSP.

- Monitor Notifications for officer queries.

- Download certificate on approval.

E. Case Law Integration

1. Re Rusape Builders (Special Court 2024)

A taxpayer with a payment plan was refused manual clearance on the basis of one missed instalment. The court held that the Commissioner’s discretion is real; refusal on a single missed instalment without consideration of the taxpayer’s overall good standing was unreasonable. ZIMRA was ordered to reconsider.

2. The proportionality principle

Maposa (2024, Lesson 3.2) on agency discipline applies by analogy: refusal of clearance must be proportionate to the alleged compliance gap.

F. Common Pitfalls

1. Skimpy “reason” field

One-line reasons get rejected. Fix: three-element formula.

2. Validity dates too long

Beyond 12 months attracts rejection. Fix: request the period actually needed.

3. Wrong attachments

Generic supporting docs raise officer queries. Fix: specific, dated, named attachments.

4. Repeated manual applications

If a taxpayer files three manual applications in a year, fix the underlying compliance gap. Fix: address the root cause.

G. Knowledge Check

Question 1

When is manual clearance appropriate vs. automatic?

Question 2

Outline the three-element formula for the “reason” field.

Question 3 — Scenario

An SME has one missed PAYE payment three months ago, since cured by a payment plan. They need clearance for a supplier-onboarding. Draft a one-paragraph “reason”.

Question 4

What does Re Rusape Builders (2024) say about refusal of manual clearance?

H. Quiz Answers with Explanations

Answer 1

Manual when automatic eligibility is not met but a certificate is genuinely needed: payment-plan-in-place, objection pending but not in default, specific tender period, single-purpose Commissioner-discretion cases.

Answer 2

Business purpose; current compliance position; bona fides.

Answer 3

Sample: “[Company] requires Tax Clearance for the period 01 May 2026–31 October 2026 to complete supplier-onboarding with [Customer], a major retailer. All tax heads are currently filed and current; April 2026 PAYE was the subject of a payment plan referenced PP-9876, fully honoured to date. Refusal of clearance would result in loss of the supplier engagement and consequent harm to revenue and tax-base.”

Answer 4

Re Rusape Builders (Special Court 2024) held that the Commissioner’s discretion to grant manual clearance is real, and refusal must be proportionate to the alleged compliance gap. Single missed instalment in an otherwise honoured plan is not adequate basis for refusal without consideration of the taxpayer’s overall good standing.

I. Key Takeaways

- Manual clearance: discretion-based exception to the “all-up-to-date” rule.

- Workflow: Taxpayer Certificates → Certificate Requests → Request for Tax Clearance (top right).

- Three-element “reason” formula: purpose, position, bona fides.

- Validity: typically up to 12 months; tender-specific often shorter.

- Rusape Builders (2024) — refusal must be proportionate.

- Continuity: Module 6 covers Single Account — the financial heart of TaRMS.