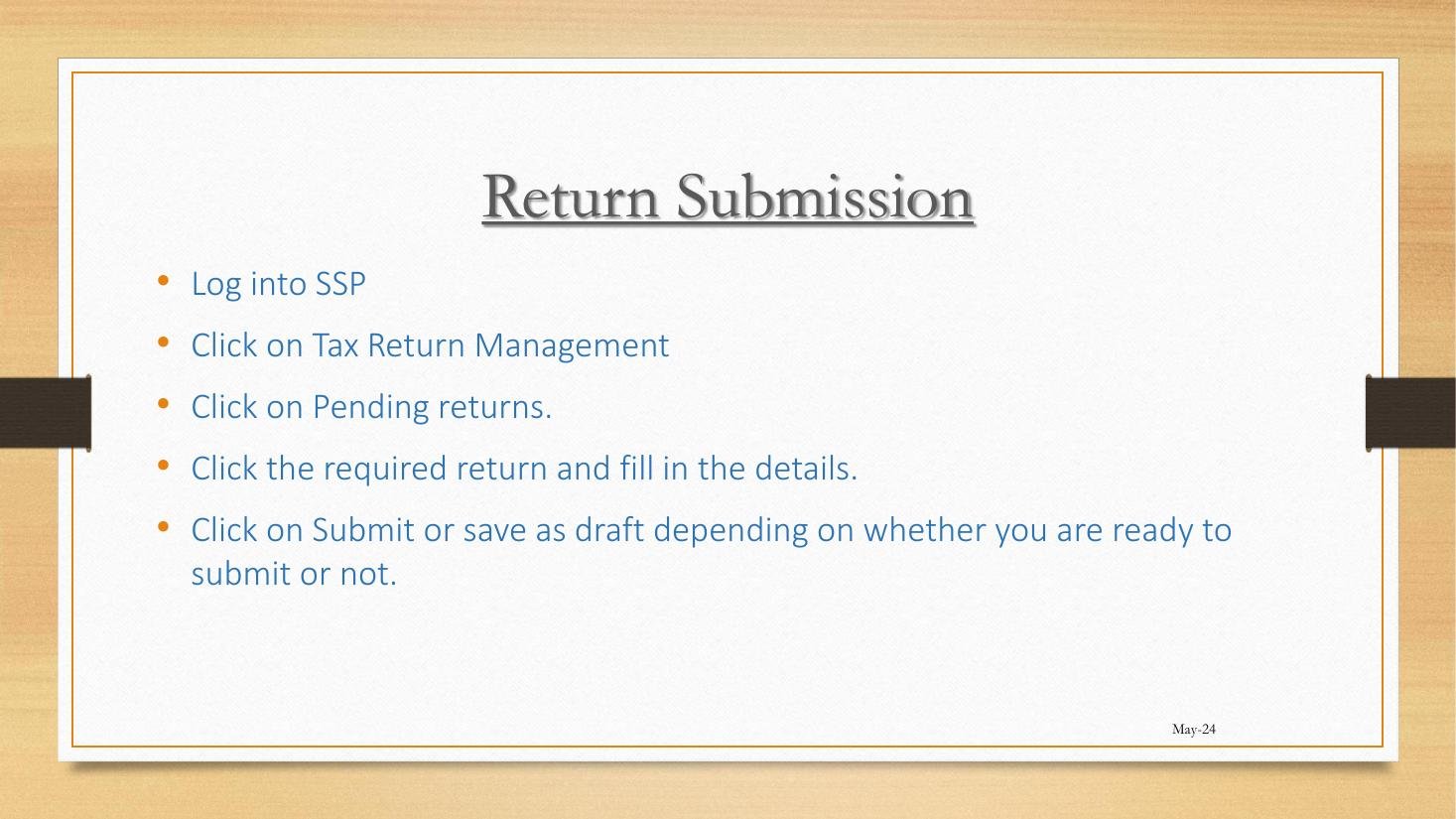

Module 4 is the heart of TaRMS Essentials — the actual filing of returns. Lesson 4.1 sets out the universal pattern that applies to every tax type: how a return is generated, how it is filled, how it is saved as a draft, how it is submitted, and how the assessment is then posted to the ledger. Lessons 4.2–4.4 then specialise: PAYE returns (4.2), current-period amendments (4.3), and back-filing of past periods (4.4).

If you can navigate Lesson 4.1, you can file any tax return on the SSP. The mechanics are uniform; only the data changes from one tax head to another.