The ITF 263 is the most-demanded ZIMRA document. Banks demand it for loans; tender boards demand it for bids; large corporates demand it for supplier onboarding; ministries demand it for licence renewals. The automatic-generation route is the reward for full compliance.

TaRMS Essentials Lesson 5.1

Automatic Tax Clearance Generation

The fast lane to an ITF 263 — one click on the Certificate Requests screen if the taxpayer is fully compliant. This lesson explains the eligibility criteria and the implications when the system refuses.

1

Executive summary

What “up-to-date” means under section 80B ITA: all returns filed, all balances settled, no audit obstructions.

2

Lesson content

The Request for Automatic Tax Clearance workflow click-by-click and how to view the certificate.

3

Assessment & policy notes

When the system refuses and what to fix to qualify.

A. Lesson Context: The Reward for Compliance

B. Legislative Framework

1. Section 80B ITA — the tax clearance regime

Establishes the certificate, sets the eligibility (all due returns filed, all due amounts paid), and prescribes the form (ITF 263).

2. Withholding-tax linkage

Section 80B is the basis for the 30% withholding-tax-on-tenders rule applied where the supplier cannot produce a current ITF 263. The receiving party is obliged to withhold and remit.

3. Validity

The certificate carries an explicit validity start and end date. Conventionally six months for automatic clearances.

4. Practice Note — the “up-to-date” test

The system computes eligibility based on the Tax Type Report (Lesson 7.2) and the Single Account balance. Zero outstanding returns + zero outstanding debt = automatic eligibility.

C. Detailed Conceptual Explanation

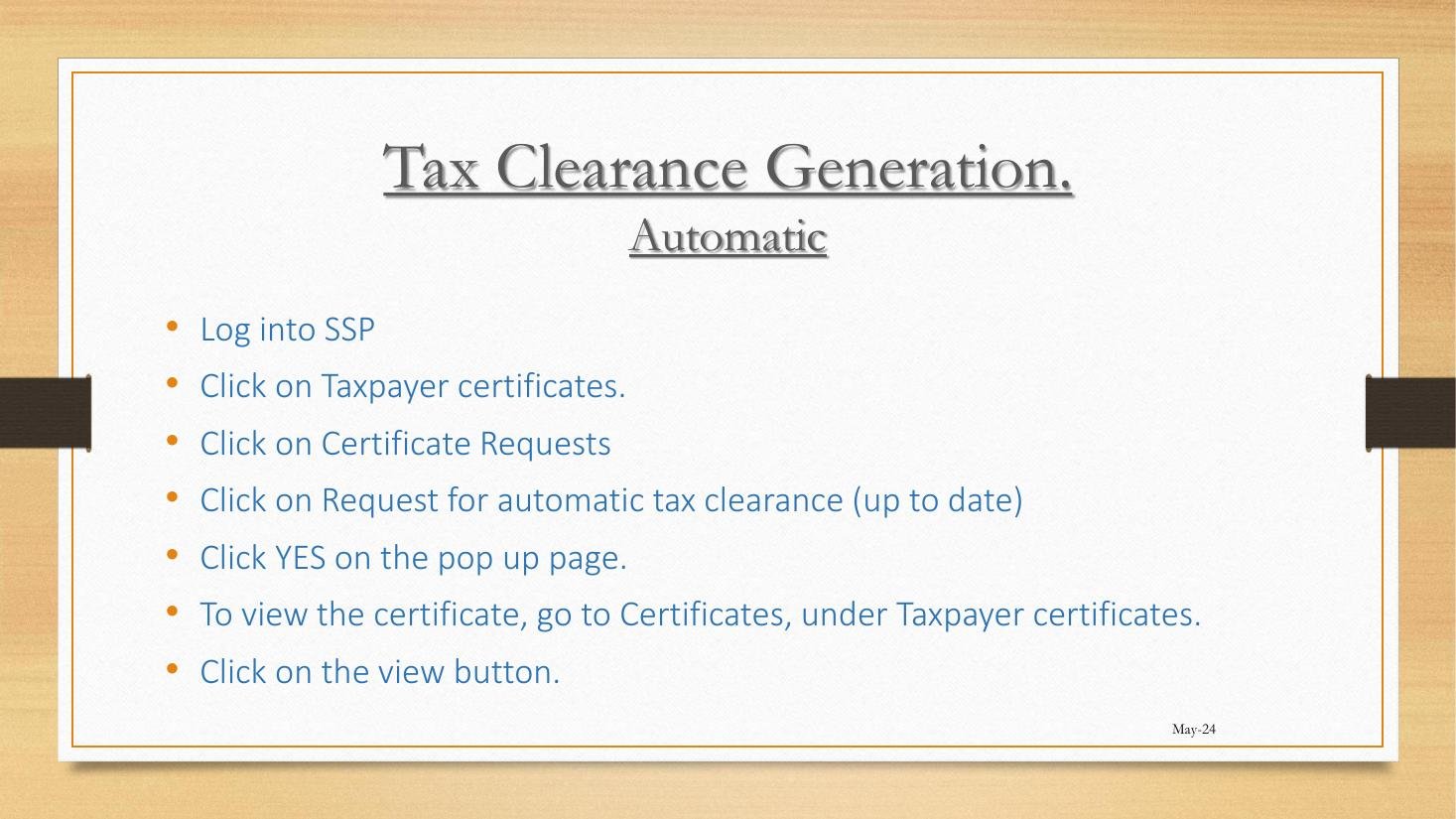

1. Workflow

- Login to SSP.

- Click Taxpayer Certificates.

- Click Certificate Requests.

- Click Request for Automatic Tax Clearance (Up to Date).

- Click Yes on the pop-up.

- To view: Taxpayer Certificates → Certificates → click View.

- Download the PDF; print or send to counterparty.

2. Eligibility test

| Condition | Required state |

|---|---|

| Outstanding returns | None |

| Outstanding debt | Zero on Single Account |

| Pending objections / appeals | None blocking |

| Audit obstructions | None flagged |

| Tax-type registrations | All current |

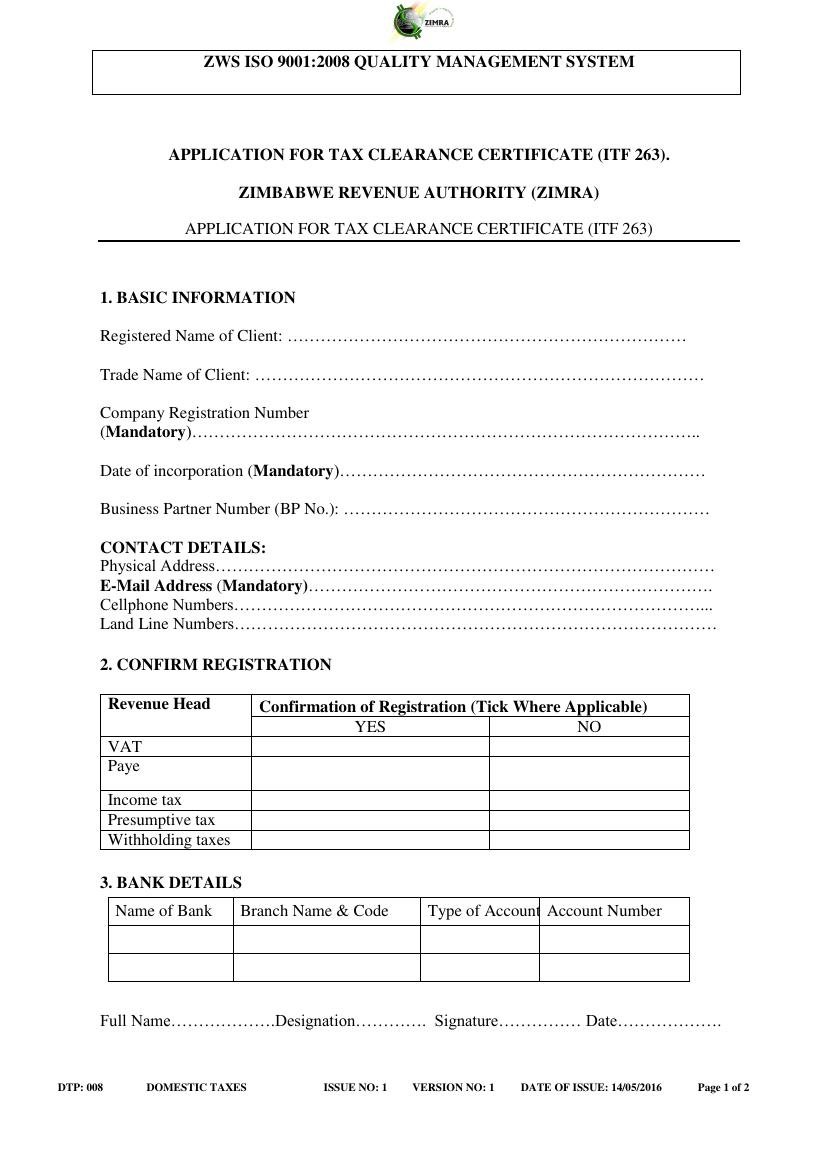

3. The legacy ITF 263 form

4. What the certificate proves

The certificate is a snapshot in time. It does not certify ongoing compliance — it certifies compliance as at the date of issue. A bank or tender board can rely on it for the validity period printed on its face.

5. Refusal and remediation

If the system refuses:

- Visit Tax Type Report — identify the head with outstanding balance.

- Visit Pending Returns — identify any unfiled returns.

- Resolve each issue, then retry.

D. Real-World Applicability

1. The bank-loan applicant

Lily applies for a kiosk-expansion loan. Bank requires a current ITF 263. She logs in, clicks Request, downloads, and submits. Total time: 2 minutes.

2. The tender bidder

Cairns Foods bids on a state-owned supply contract. The procurement officer requires ITF 263 dated within 30 days. The tax team requests fresh on tender day; submitted with the bid.

3. The supplier-onboarding case

OK Zimbabwe onboards a new supplier; demands ITF 263 each year on contract renewal. Annual download; filed in the supplier portal.

4. The 30%-withholding-tax interaction

A supplier cannot produce ITF 263. The buyer must withhold 30% of the contract value as withholding tax and remit to ZIMRA. The supplier’s motivation to maintain ITF 263 is therefore commercial as well as compliance-based.

E. Case Law Integration

1. Public Procurement Authority v. Tinotenda Suppliers (High Court 2022)

A bidder lost a tender for failure to produce a current ITF 263. The court upheld the procurement decision — a procurement officer is entitled to insist on current clearance.

2. Section 80B compliance challenges

A series of unreported Special Court matters confirm that a single late return blocks automatic clearance — ZIMRA’s practice notes do not allow waiver of the “up-to-date” test.

F. Common Pitfalls

1. Treating the certificate as “always available”

If a return slips, the system refuses. Fix: file before requesting.

2. Using a stale certificate

Banks demand fresh; download on the day of submission.

3. Ignoring system refusal

The refusal message names the obstacle. Fix the obstacle, not the certificate request.

4. Forgetting the 30%-withholding consequence

Lack of ITF 263 costs 30% of contract value. Fix: compliance is cheaper.

5. Confusing automatic with manual

Automatic = full compliance. Manual = exceptional case (Lesson 5.2).

G. Knowledge Check

Question 1

State the section 80B test for automatic tax clearance.

Question 2

Walk through the seven-step request workflow.

Question 3 — Scenario

You request automatic clearance and the system refuses. What is the correct response?

Question 4

Why does a supplier without ITF 263 face a 30% withholding consequence on a tender?

H. Quiz Answers with Explanations

Answer 1

All due returns filed; all due amounts paid; no blocking objections, appeals, or audit flags. Section 80B ITA. The system computes eligibility automatically.

Answer 2

(1) Login. (2) Taxpayer Certificates. (3) Certificate Requests. (4) Request for Automatic Tax Clearance (Up to Date). (5) Yes on pop-up. (6) Certificates section. (7) View / Download.

Answer 3

Read the refusal message; visit Tax Type Report and Pending Returns to identify the specific obstacle; remediate (file return, settle balance); retry. Do not attempt to bypass via the manual workflow (Lesson 5.2) unless the obstacle is genuinely beyond automatic remediation.

Answer 4

Section 80B and related provisions impose a withholding obligation on the buyer where the supplier cannot produce ITF 263 — 30% of contract value is deducted and remitted to ZIMRA. The supplier’s lack of clearance therefore costs them 30% upfront, recoverable only via subsequent assessment if at all.

I. Key Takeaways

- Automatic = full compliance reward.

- Workflow: Taxpayer Certificates → Certificate Requests → Request for Automatic.

- Eligibility = zero unfiled returns + zero outstanding debt.

- 30%-withholding consequence on tenders without ITF 263.

- Continuity: Lesson 5.2 covers manual application when automatic is unavailable.