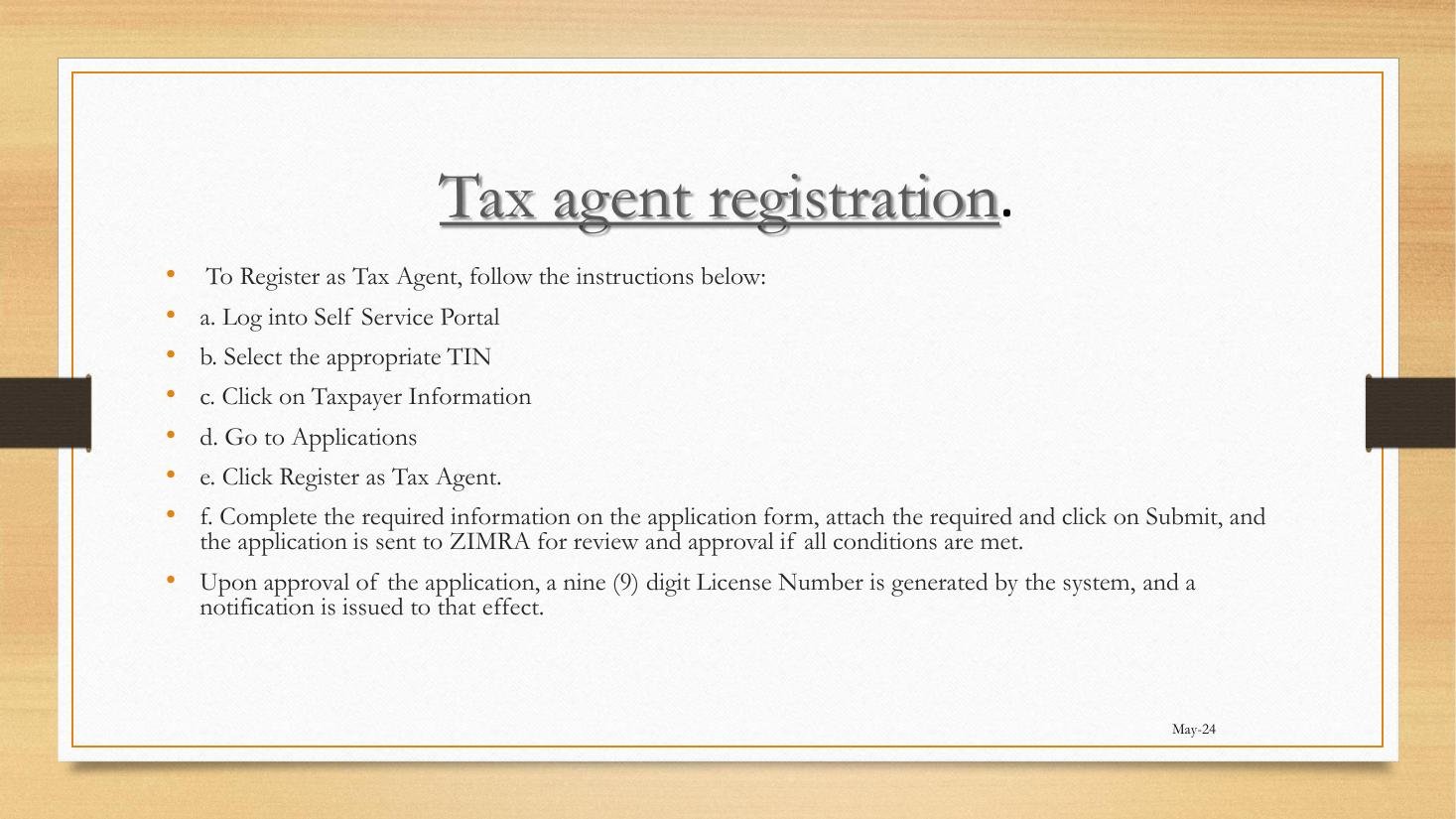

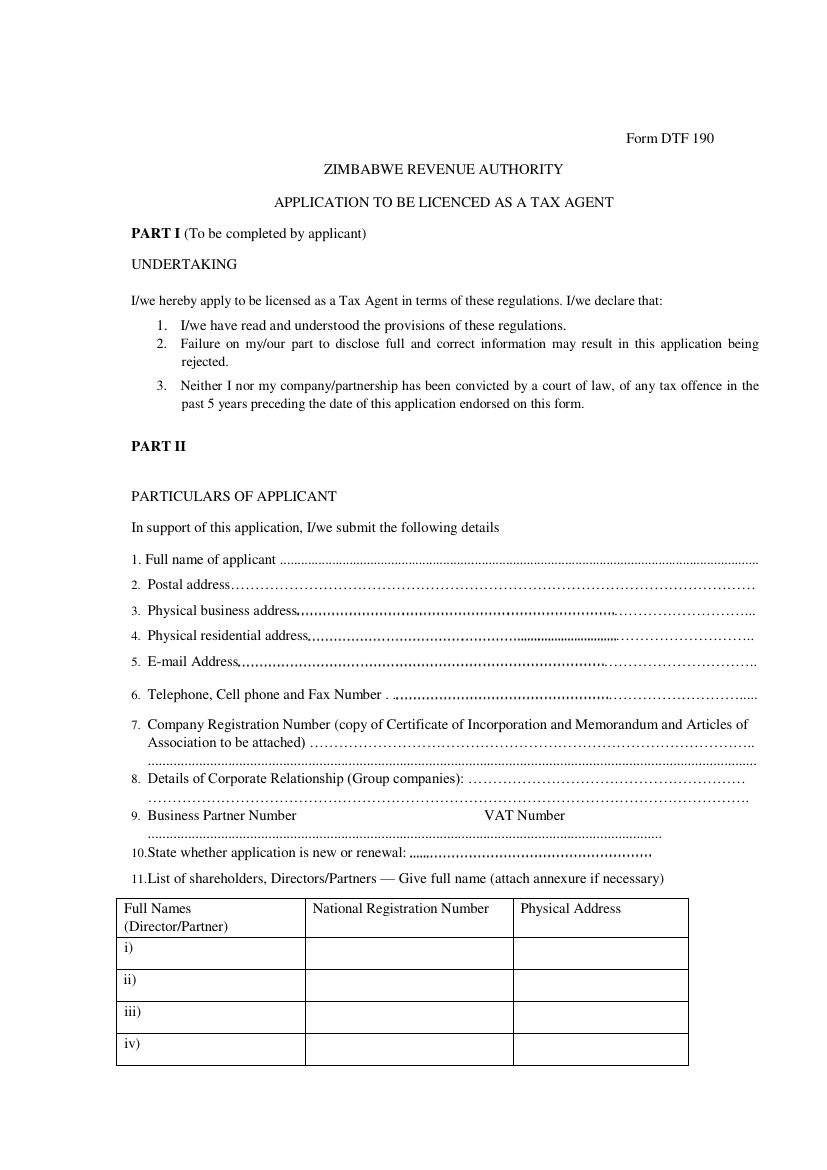

Before October 2023, anyone with a passable understanding of tax could call themselves a “tax agent” in Zimbabwe and lodge returns on a client’s behalf using shared credentials. Statutory Instrument 125 of 2023 — the Tax Agent (Licensing) Regulations — ended that. Today, every individual or firm transacting on another person’s TIN must be licensed by ZIMRA, hold a 9-digit Licence Number, and operate inside the controls Module 3 sets up.

This is the gateway lesson for Module 3. Lesson 3.2 will treat licence management; Lesson 3.3 will cover the assignment of an agent to a client TIN; Lesson 3.4 will explain how an agent firm structures internal access via Roles and Assignees. Get Lesson 3.1 right and the rest of the module is execution.

Why this matters commercially: A Tax Agent licence is the asset that allows a firm to scale beyond a sole-trader practice. Without it, every additional client requires the firm to share their own SSP credentials — a practice that is now unlawful and uninsurable.