Every employer in Zimbabwe with one or more employees files a PAYE return monthly. The volume of PAYE returns dwarfs every other return type, and the volume of PAYE-related help-desk queries dwarfs every other category. This lesson goes deep on the mechanics so the practitioner can be the help-desk-call avoider, not the help-desk-call generator.

TaRMS Essentials Lesson 4.2

PAYE Return Submission

The PAYE return is the most filed return in Zimbabwe — monthly, with a strict template, dual-currency capability, and an unforgiving parser. This lesson teaches the workflow, the template discipline, and back-filing of pre-2024 periods.

1

Executive summary

The PAYE legal framework, P2 return form, and the rules on dual-currency reporting introduced by the Finance Act 2025.

2

Lesson content

The submission workflow, the standard template (do not alter the headings), and the post-January 2024 vs. pre-January 2024 filing rules.

3

Assessment & policy notes

Common PAYE template errors, knowledge-check questions, and a monthly PAYE-day playbook.

A. Lesson Context: PAYE is the High-Volume Return

B. Legislative Framework

1. Sections 73–79 Income Tax Act

The PAYE regime: employer’s duty to deduct, monthly remittance, the P2 return, certificates of tax deducted (P6), and the year-end reconciliation.

2. Section 73 — due date

The P2 return and the PAYE remittance are due within 10 days of the close of each month.

3. Finance Act 2025 — dual-currency PAYE

Where employees are remunerated in both ZWG and USD, the employer must declare PAYE in both currencies on a single return using the dual-currency option.

4. Penalties

Late submission: civil penalty per the schedule. Late remittance: interest at the prescribed rate. Wilful non-deduction: criminal liability under section 80 ITA.

5. Practice Note — PAYE template

The PAYE upload template is published by ZIMRA. Headings must not be altered. The parser is exact-match.

C. Detailed Conceptual Explanation

1. The submission workflow

- Login to SSP → Tax Return Management → Pending Returns.

- Open the PAYE return for the relevant month.

- Currency Selection: select USD, ZWG, or both, matching the actual currency of remuneration.

- Download the PAYE template provided on the return screen.

- Fill in the template — one row per employee — without altering the headings.

- Upload the completed template back to the return screen.

- Verify totals; resolve any validation errors.

- Submit (or Save as Draft).

2. The PAYE template structure

| Column | Content |

|---|---|

| National ID / TIN | Employee identifier |

| First Name / Surname | As on ID |

| Gross Remuneration | Total taxable employment income |

| Allowable Deductions | Pension, Aids Levy, allowable deductions |

| Taxable Income | Gross minus allowables |

| PAYE Deducted | Tax actually deducted from the employee |

| Currency | USD or ZWG |

| Branch | Where the employee is allocated |

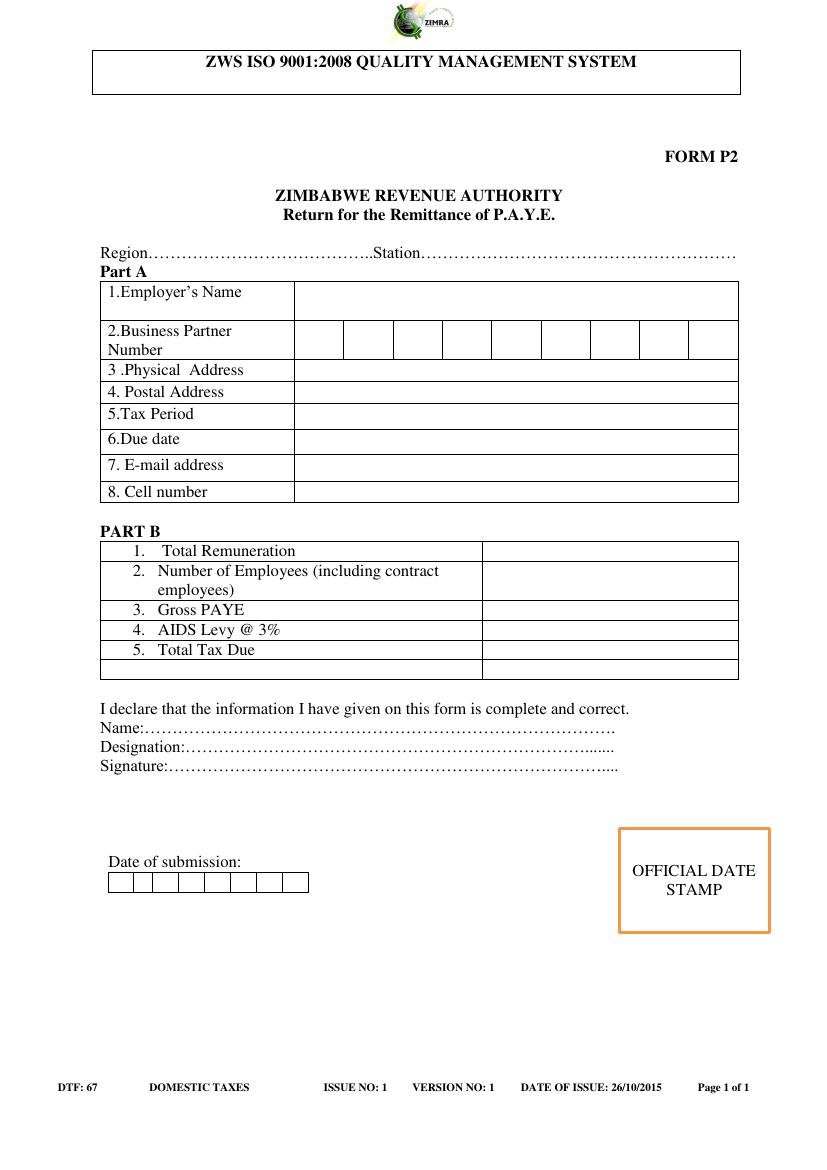

3. The legacy P2 paper form — what it tells you

4. Pre-January 2024 vs. post-January 2024 rules

For PAYE periods from January 2024 onward, the full template must be completed with employee detail. For prior missing periods, ZIMRA accepts a blank template (without altering headings) accompanied by the aggregate PAYE total. This is a transitional concession arising from the migration; do not extend the practice to current periods.

5. Currency selection logic

| Remuneration pattern | Currency Selection |

|---|---|

| All employees paid in USD only | USD |

| All employees paid in ZWG only | ZWG |

| Mixed: some employees USD, some ZWG, or each in both | ZWG and USD (dual) |

6. The dual-currency return

Under the Finance Act 2025 dual-currency regime, the template includes a Currency column on every row. The system aggregates per currency and produces two separate liability figures, settled separately through the Single Account.

7. Year-end reconciliation

P2 monthly returns are reconciled to year-end via the P6 (employee-level certificate) and the ITF 16 employer’s annual return. Mismatches between monthly P2 totals and the year-end reconciliation are a routine ZIMRA audit-trigger.

8. Aids Levy

3% of PAYE (effectively a surcharge on the tax). The template captures it implicitly via the PAYE-deducted column — ensure the levy is included.

D. Real-World Applicability

1. The 2-employee SME (Lily, post-VAT registration)

Lily hires two staff in mid-2026. Her monthly PAYE workflow:

- End of month: payroll computed in her bookkeeping software.

- Day 5 of new month: log into SSP, open Pending Return for PAYE.

- Select USD (her two staff are paid in USD).

- Download template, populate two rows.

- Upload, validate, submit.

- Pay PAYE liability via Single Account.

2. The 200-employee corporate

The payroll system exports the PAYE template directly. The Tax Manager reviews the export, uploads to SSP, runs the validation, fixes any errors (typically: a new joiner without TIN), and submits. Total time on the SSP: 15 minutes.

3. The agent serving multiple SME clients

An agent runs PAYE for 12 SME clients. Her process: switch to Client 1, file PAYE; switch to Client 2; etc. With practice she completes all 12 in under 2 hours on the day of deadline.

4. The PAYE-day playbook

- Day 1 of new month: payroll closes; numbers locked.

- Day 2–5: payroll team produces PAYE template per Lesson 4.2 schema.

- Day 6: tax team reviews template for completeness.

- Day 7: SSP submission — one currency at a time if dual.

- Day 7: Single Account remittance.

- Day 8–10: monitoring of acknowledgement and Tax Type Report.

E. Case Law Integration

1. Innscor Africa v. Commissioner-General, ZIMRA (Special Court 2019)

A large employer’s PAYE template was rejected by the parser due to a renamed heading (“EmployeeID” instead of “National ID / TIN”). ZIMRA issued late-submission penalty. The court upheld the penalty: the obligation is to lodge in the prescribed format; format-deviance is non-compliance.

2. Triangle Sugar v. Commissioner-General (Special Court 2021)

Pre-dual-currency, an employer paying a small US-dollar component to a few employees attempted to file in ZWG only. Section 80 ITA exposure; settlement reached. The Finance Act 2025 dual-currency regime resolved the conceptual ambiguity prospectively.

3. Re Borrowdale Boutique (Magistrates’ Court 2024)

An employer wilfully under-declared PAYE for 14 months. Section 80 conviction; fine plus full back-payment. The PAYE history-tab (Lesson 7.x) was the primary evidence.

F. Common Pitfalls

1. Altered template headings

Innscor Africa (2019). Never edit the headings.

2. Wrong currency selection

Triggers an audit. Match selection to actual remuneration currency.

3. Missing TINs for new joiners

Each employee must have a TIN. Fix: have HR ensure new joiners obtain a TIN within their first week.

4. Treating year-end reconciliation as optional

The ITF 16 reconciles monthly P2 totals; mismatches trigger audit. Fix: reconcile monthly, not annually.

5. Forgetting the Aids Levy 3%

It is part of PAYE deducted. Fix: ensure payroll software calculates and includes it.

6. Filing in February for January at 23:59 on day 10

System risk. Submit by day 7.

7. Treating expat employees on USD-only as exempt from ZWG reporting

If they are also paid any ZWG component, the dual-currency return applies.

G. Knowledge Check

Question 1

What is the PAYE due date and what is its statutory authority?

Question 2

What are the eight columns in the standard PAYE template? What happens if a column heading is renamed?

Question 3 — Scenario

An SME has 5 employees: 3 paid in USD only, 2 paid 60% USD / 40% ZWG. What currency selection should the employer choose, and how does the template reflect the mixed pay?

Question 4 — Scenario

An employer realises after submission that they omitted one employee’s PAYE for the month. What is the correct fix — amendment now or include in next month’s return?

Question 5

Outline the PAYE-day playbook from Day 1 to Day 10.

H. Quiz Answers with Explanations

Answer 1

Within 10 days of the close of each month, per section 73 of the Income Tax Act [Chapter 23:06], read with the relevant sub-sections governing the P2 return and remittance.

Answer 2

National ID / TIN, First Name, Surname, Gross Remuneration, Allowable Deductions, Taxable Income, PAYE Deducted, Currency, and (added) Branch. Renaming a heading breaks the parser; the return is rejected as non-conforming. Innscor Africa (2019) confirms the rule.

Answer 3

Currency Selection: ZWG and USD (dual). The template shows one row per employee per currency portion (or the dual-currency variant captures both on one row). The 3 USD-only employees: one row each, Currency = USD. The 2 mixed employees: two rows each, one with their USD portion and one with their ZWG portion, OR the dual-currency template with both columns populated. Total liability is computed and remitted separately for each currency.

Answer 4

The cleanest fix is the Amend workflow on Submitted Returns (Lesson 4.3) for the current period — add the missing employee, re-validate, re-submit. Including in next month’s return is wrong because (i) it understates this month’s liability, attracting interest; (ii) the year-end reconciliation will not balance; (iii) the employee’s P6 will be incorrect for the period.

Answer 5

Day 1: payroll closes. Day 2–5: produce template. Day 6: tax-team review. Day 7: SSP submission and Single Account remittance. Day 8–10: monitor acknowledgement and Tax Type Report. Resist the temptation to push to day 10 itself; system risk is unforgiving.

I. Key Takeaways

- PAYE due within 10 days of month-end; section 73 ITA.

- Template headings are sacred — never rename them.

- Dual-currency reporting under Finance Act 2025 for mixed remuneration.

- Aids Levy 3% included within PAYE deducted.

- Year-end reconciliation via ITF 16 = audit trigger if mismatched.

- Submit by day 7, not day 10.

- Continuity: Lesson 4.3 next handles current-period amendments — the route to fix the inevitable post-submission errors.