The bank holding the Single Account matters: forex spreads, transaction fees, branch coverage, and digital-banking integration all vary. Lesson 6.2 walks through the change workflow and the operational discipline needed during transition.

TaRMS Essentials Lesson 6.2

Changing the Single Account Bank

When a taxpayer wants to switch their nominated bank for the Single Account — the workflow, the lag before the new bank takes effect, and the reconciliation discipline during transition.

1

Executive summary

Why a taxpayer might change banks (rate, service, geographic spread); the SSP Change Single Account workflow.

2

Lesson content

The transition lag, in-flight payment reconciliation, and the cleanest payment-pause window.

3

Assessment & policy notes

Common transition pitfalls and a bank-switching playbook.

A. Lesson Context: Bank Choice as a Strategic Decision

B. Legislative Framework

1. Section 34B RAA — Commissioner’s prescribed banks

ZIMRA publishes a list of approved banks; only these may host a Single Account.

2. Practice Note on Bank Changes

ZIMRA Public Notice 4 of 2024 sets the standard transition: the new bank is effective from the first day of the next tax period after approval; in-flight payments to the old bank during the transition window are honoured.

3. Cyber and Data Protection Act

The change of bank involves transfer of taxpayer banking details; the Cyber Act’s data-protection rules apply.

C. Detailed Conceptual Explanation

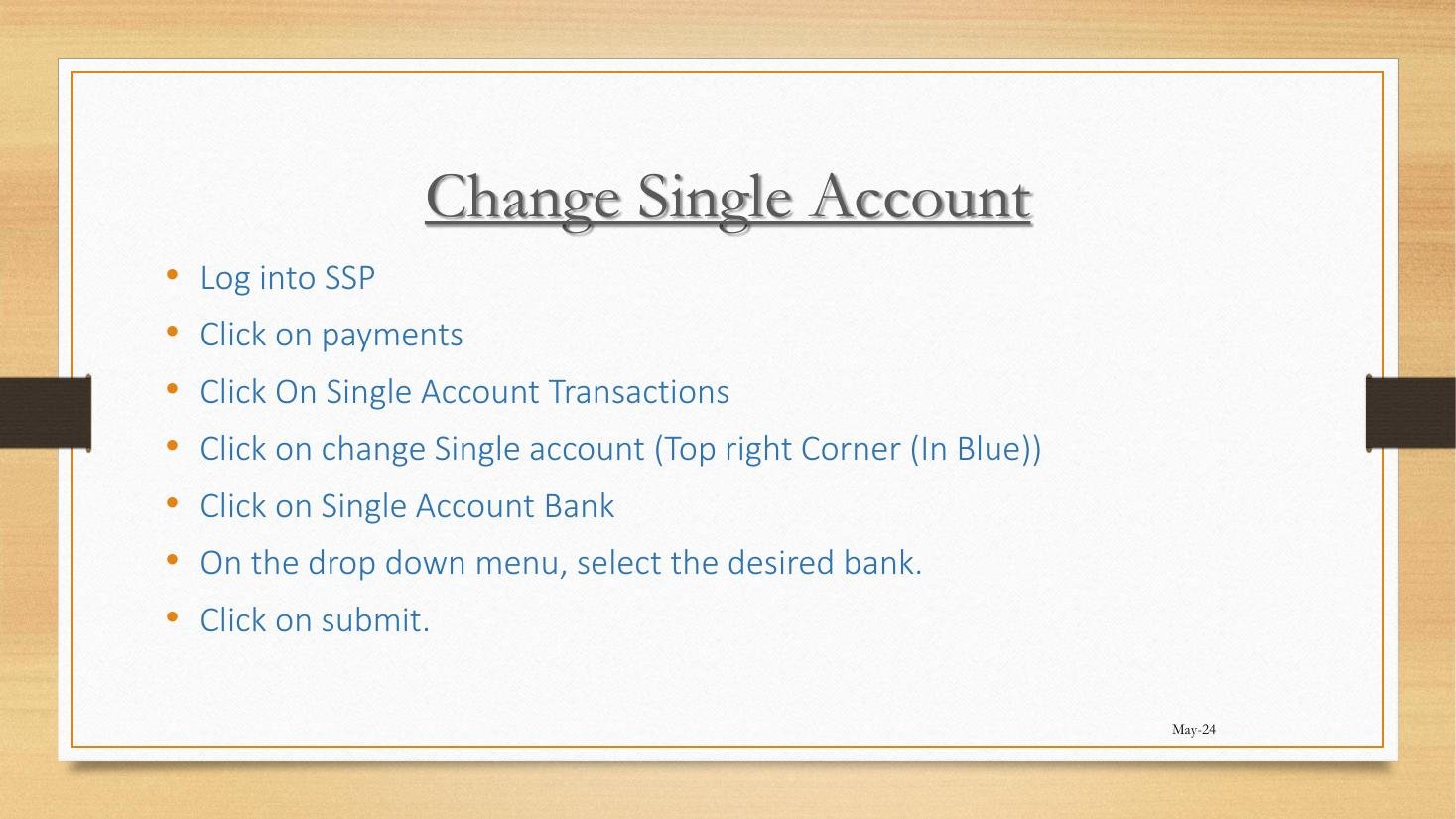

1. Seven-step workflow

- Login to SSP.

- Click Payments.

- Click Single Account Transactions.

- Click Change Single Account (top right, blue).

- Click Single Account Bank.

- From the drop-down, select the desired bank.

- Click Submit.

2. Approval and the lag

ZIMRA validates the new bank choice; processing 5–10 working days. New bank effective from the first day of the next tax period after approval.

3. The transition window discipline

- Pause non-urgent payments during the transition window.

- Continue paying urgent obligations to the old bank until effectivity.

- On effectivity, redirect all bank instructions to the new bank.

- Reconcile both banks for the next 30 days.

4. The bank-list considerations

| Factor | Question to ask |

|---|---|

| Forex spreads | What does the bank charge on USD-ZWG conversion? |

| Transaction fees | Per-transfer fee structure, especially for high-volume payers. |

| Branch network | Geographic spread for cash-deposit needs. |

| Digital-banking integration | Does the bank’s API integrate with the taxpayer’s ERP? |

| Service level | Speed of clearing for ZIMRA-bound transfers. |

D. Real-World Applicability

1. The corporate switching for forex

Cairns Foods’ finance team analyses forex spreads across the approved-bank list and chooses the best. They lodge change request; effective from start of next quarter.

2. The SME with a service complaint

Lily’s current bank’s clearing is slow; she switches. Process is identical regardless of size.

3. The agent-managed transition

An agent advising a client through a switch coordinates the transition window with the client’s cash-flow team to avoid mid-period confusion.

E. Case Law Integration

1. Re Mutare Manufacturing (Special Court 2024)

A taxpayer’s payment was sent to the old bank during transition; ZIMRA initially treated it as unallocated. The court held that the Practice Note on Bank Changes contemplates the transition window and that in-flight payments to the old bank are honoured. Allocation accepted.

F. Common Pitfalls

1. Switching mid-period

Reconciliation pain. Fix: time switches to start of next tax period.

2. Not informing internal payment teams

Payments continue to old bank. Fix: internal communication on effectivity.

3. Choosing on price alone

Service matters. Fix: evaluate on full criteria.

4. Forgetting the new RefNum / Account details

Bank instruction templates need updating. Fix: on effectivity, update all banking templates.

G. Knowledge Check

Question 1

Walk through the seven-step Change Single Account Bank workflow.

Question 2

What is the typical lag between submission and effectivity?

Question 3 — Scenario

You lodge change request 12 March; ZIMRA approves 19 March. When does the new bank become effective for a Category C VAT-registered taxpayer?

Question 4

What does Re Mutare Manufacturing (2024) say about in-flight payments during transition?

H. Quiz Answers with Explanations

Answer 1

Login → Payments → Single Account Transactions → Change Single Account → Single Account Bank → choose bank → Submit.

Answer 2

5–10 working days for ZIMRA processing; effective from first day of next tax period after approval.

Answer 3

For a Category C (monthly) VAT taxpayer, the next tax period starts 1 April. The new bank is effective from 1 April. Pre-1 April payments go to the old bank; post-1 April payments to the new.

Answer 4

The Practice Note on Bank Changes contemplates the transition window. In-flight payments to the old bank during the transition are honoured. Re Mutare Manufacturing (Special Court 2024) confirms allocation acceptance for old-bank in-flight payments.

I. Key Takeaways

- Workflow: Payments → Single Account Transactions → Change Single Account.

- 5–10 working day approval; effective from start of next tax period.

- Transition window: in-flight payments to old bank are honoured.

- Choose bank on full criteria, not price alone.

- Continuity: Lesson 6.3 next teaches transaction search and export.