The Summary Report is a Tax Manager’s first screen each morning. It aggregates the consolidated position across every registered tax head and both currencies, and surfaces any non-zero balance that requires attention. Lessons 7.2 and 7.3 then drill into the underlying detail.

TaRMS Essentials Lesson 7.1

The Summary Report

The single-screen consolidated view of every taxpayer obligation across every tax head and both currencies — the screen a Tax Manager looks at first thing every morning.

1

Executive summary

What the Summary Report aggregates and how it relates to the Tax Type Report and Assessment Notices.

2

Lesson content

Workflow, columns, currency segregation, and reading non-zero balances.

3

Assessment & policy notes

Common Summary-Report misreadings and a daily-monitoring playbook.

A. Lesson Context: The Daily Health Check

B. Legislative Framework

1. Section 51 ITA — record retention

The Summary Report is part of the digital record retained by ZIMRA.

2. Section 80B — tax clearance dependence

An automatic tax clearance request consults the Summary Report’s zero-balance condition.

3. Section 79A — allocation logic feeding the Summary

The priority rules in s. 79A determine how Single Account inflows reduce the balances visible on the Summary.

C. Detailed Conceptual Explanation

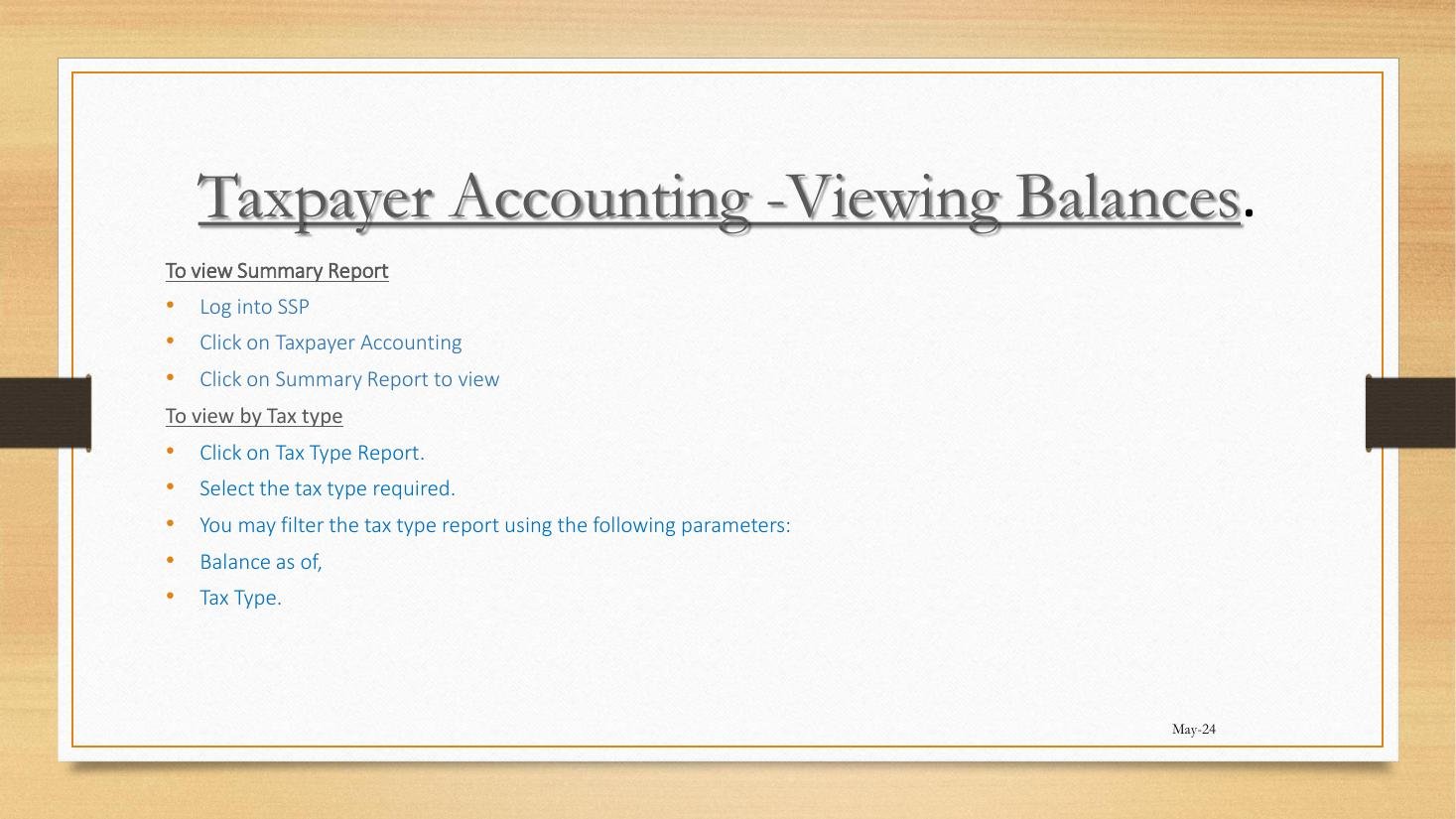

1. Workflow

- Login to SSP.

- Click Taxpayer Accounting.

- Click Summary Report.

- The consolidated view loads.

2. What the Summary aggregates

| Column | Meaning |

|---|---|

| Tax Type | Each registered head listed. |

| Principal Amount Due | Substantive tax liability. |

| Overdue Amount Due | Past-due principal. |

| Interest | Accrued interest under prescribed rate. |

| Penalties | Civil penalties levied. |

| Total Payable Amount | Sum of the above. |

| (All split by currency) | ZWG and USD sub-columns. |

3. Reading a non-zero balance

- If only Principal: Recent assessment, not yet paid — pay if due.

- If Overdue: Past-due liability — immediate attention; interest accruing.

- If Interest only: Past-due that has been recently part-settled; ensure full settlement.

- If Penalty: Compliance lapse triggered penalty; consider objection if disputed.

4. Relationship to other reports

flowchart LR

RET["Returns submitted"] --> ASS["Assessment Notices"]

ASS --> TYR["Tax Type Report"]

TYR --> SUM["Summary Report"]

SA["Single Account payments"] --> SUM

5. The daily-monitoring playbook

- Open Summary Report.

- Note any non-zero rows.

- For each non-zero, drill via Tax Type Report (Lesson 7.2) for detail.

- For surprising assessments, open Assessment Notices (Lesson 7.3).

- Action: pay, object, or query.

D. Real-World Applicability

1. The Tax Manager’s morning

5-minute scan of Summary Report; any non-zero is investigated immediately.

2. The agent’s portfolio view

For each client TIN switched to, glance at Summary; aggregate any concerning balances into a portfolio-level briefing.

3. The pre-clearance check

Before requesting Tax Clearance (Module 5), confirm Summary shows zero across all heads.

E. Case Law Integration

1. Evidentiary use

The Summary Report is a state document admissible under section 4 Civil Evidence Act. Practitioners include screenshots in objection bundles.

2. Section 47 ITA reach-back

The Summary shows current balances, not historical; for reach-back work, use Tax Type Report with date filter.

F. Common Pitfalls

1. Reading totals across currencies

ZWG and USD do not net. Fix: read each currency separately.

2. Treating zero Summary as full compliance

Summary captures balance, not unfiled returns. Fix: check Pending Returns separately.

3. Acting on Summary without drilling

Aggregate hides drivers. Fix: use Tax Type Report for detail.

G. Knowledge Check

Question 1

What columns does the Summary Report carry?

Question 2

Distinguish a non-zero Principal balance from a non-zero Penalty balance.

Question 3 — Scenario

Summary shows USD 0 across all heads, but Pending Returns shows 1 unfiled VAT return. Are you compliant?

H. Quiz Answers with Explanations

Answer 1

Tax Type, Principal, Overdue, Interest, Penalties, Total Payable — all per currency.

Answer 2

Principal = substantive tax assessed but unpaid. Penalty = civil-penalty levy for compliance lapse. Both require action; the latter may be the basis for objection if penalty was wrongly applied.

Answer 3

No. Compliance is two-sided: balance and filing. Zero balance with unfiled returns is not full compliance. Tax Clearance will be refused. Fix: file the VAT return; balance may then update if the return generates liability.

I. Key Takeaways

- Summary Report = consolidated daily health check.

- Six columns, two currencies; never net across currencies.

- Pair with Pending Returns for full compliance picture.

- Drill via Tax Type Report (Lesson 7.2) for detail.

- Continuity: Lesson 7.2 covers the Tax Type Report.