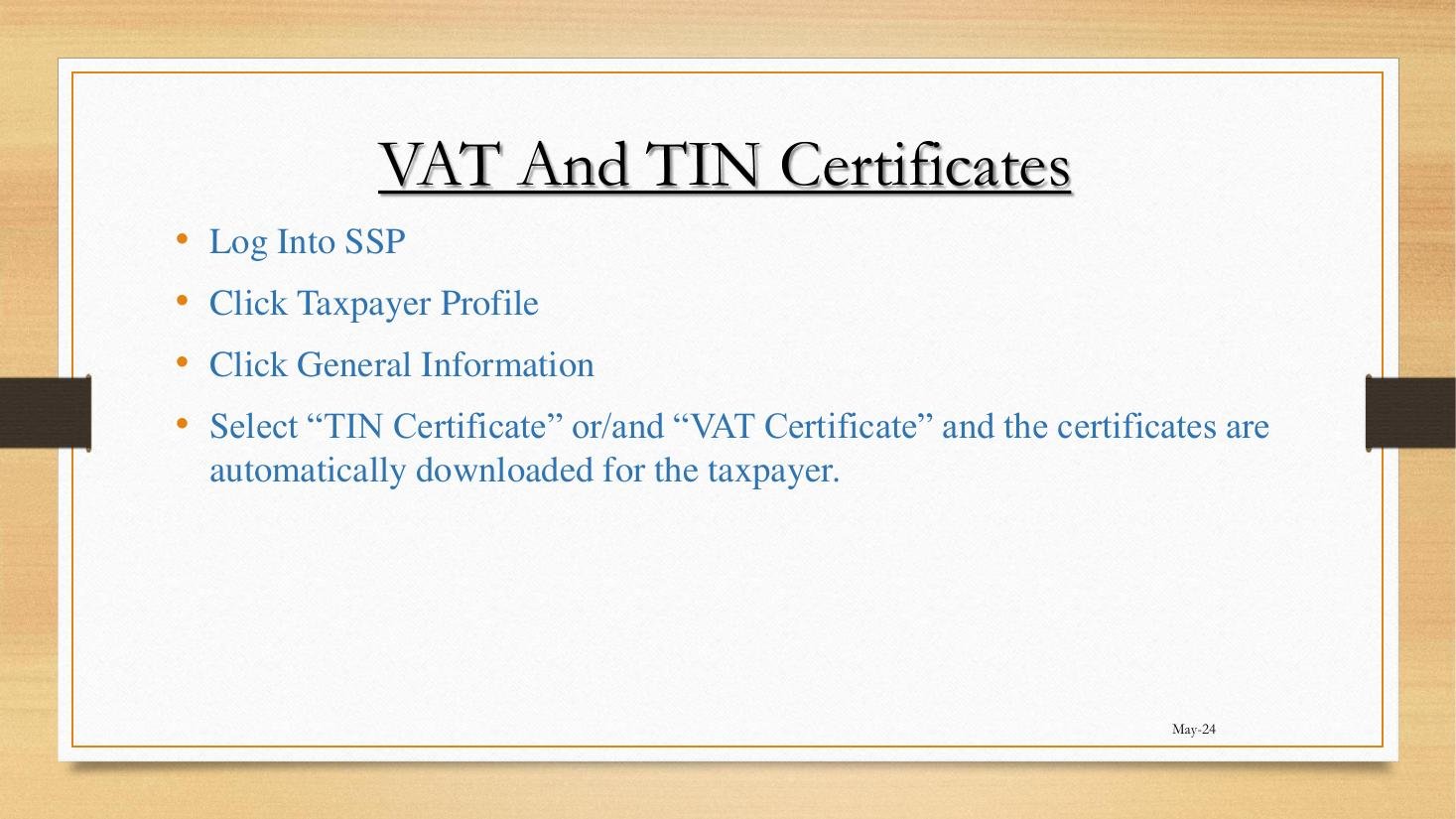

A Zimbabwean taxpayer encounters three distinct certificates issued by ZIMRA in routine business life: the TIN Certificate, the VAT Certificate, and the Tax Clearance Certificate (ITF 263). They look superficially similar — ZIMRA letterhead, taxpayer name, TIN, a digital signature panel — but they serve fundamentally different purposes, and bankers, lawyers, and procurement officers are inconsistent in which one they ask for.

This short lesson serves three functions. It teaches the simplest action on the SSP (downloading TIN/VAT certificates) as a confidence-building exercise. It clarifies the difference between the three certificates so the learner does not waste time fetching the wrong one. And it lays the groundwork for Module 5 (Tax Clearance Certificates), which is altogether more involved.