Newly-engaged tax practitioners frequently inherit clients with gaps in their filing history — a PAYE return missed during a system outage, a VAT return overlooked during ownership change, a presumptive-tax period skipped during the TaRMS migration. Lesson 4.4 teaches the back-filing workflow and the Voluntary Disclosure overlay that softens the penalty consequence.

TaRMS Essentials Lesson 4.4

Filing Past Returns and Back-Filing

When a return for an old period was never filed, TaRMS does not always auto-generate a Pending Return. The New Tax Return workflow on Submitted Returns is the route — with a six-year statutory window and Voluntary Disclosure overlay.

1

Executive summary

The legal window for back-filing (section 47 ITA), the role of Voluntary Disclosure (VDA01), and ZIMRA’s administrative practice.

2

Lesson content

The New Tax Return workflow on Submitted Returns; how to choose period; what to attach.

3

Assessment & policy notes

Common back-filing pitfalls, knowledge-check questions, and a chronological-cleanup playbook.

A. Lesson Context: Cleaning Up the Past

B. Legislative Framework

1. Section 47 ITA — six-year reach-back

ZIMRA may assess additional tax for any of the past six years. The taxpayer therefore has a corresponding ability to back-file for the same window without statute-bar consequences on either side.

2. Voluntary Disclosure under VDA01

The Voluntary Disclosure Application (VDA01) form allows a taxpayer to disclose past non-compliance proactively. Penalty mitigation typically: full waiver if disclosure precedes any audit selection; partial waiver if disclosed during audit but before assessment.

3. Finance Bill 2026

The Bill proposes tightening the back-filing window for PAYE specifically — potentially three years rather than six — with corresponding increases in penalty for older missed returns.

4. Section 80 ITA

Wilful non-filing is a section 80 offence. Voluntary back-filing converts the offence to administrative non-compliance.

5. Practice Note on Back-Filing

ZIMRA Public Notice 7 of 2024 sets out the standard process: file via the New Tax Return workflow with a covering memorandum explaining the omission.

C. Detailed Conceptual Explanation

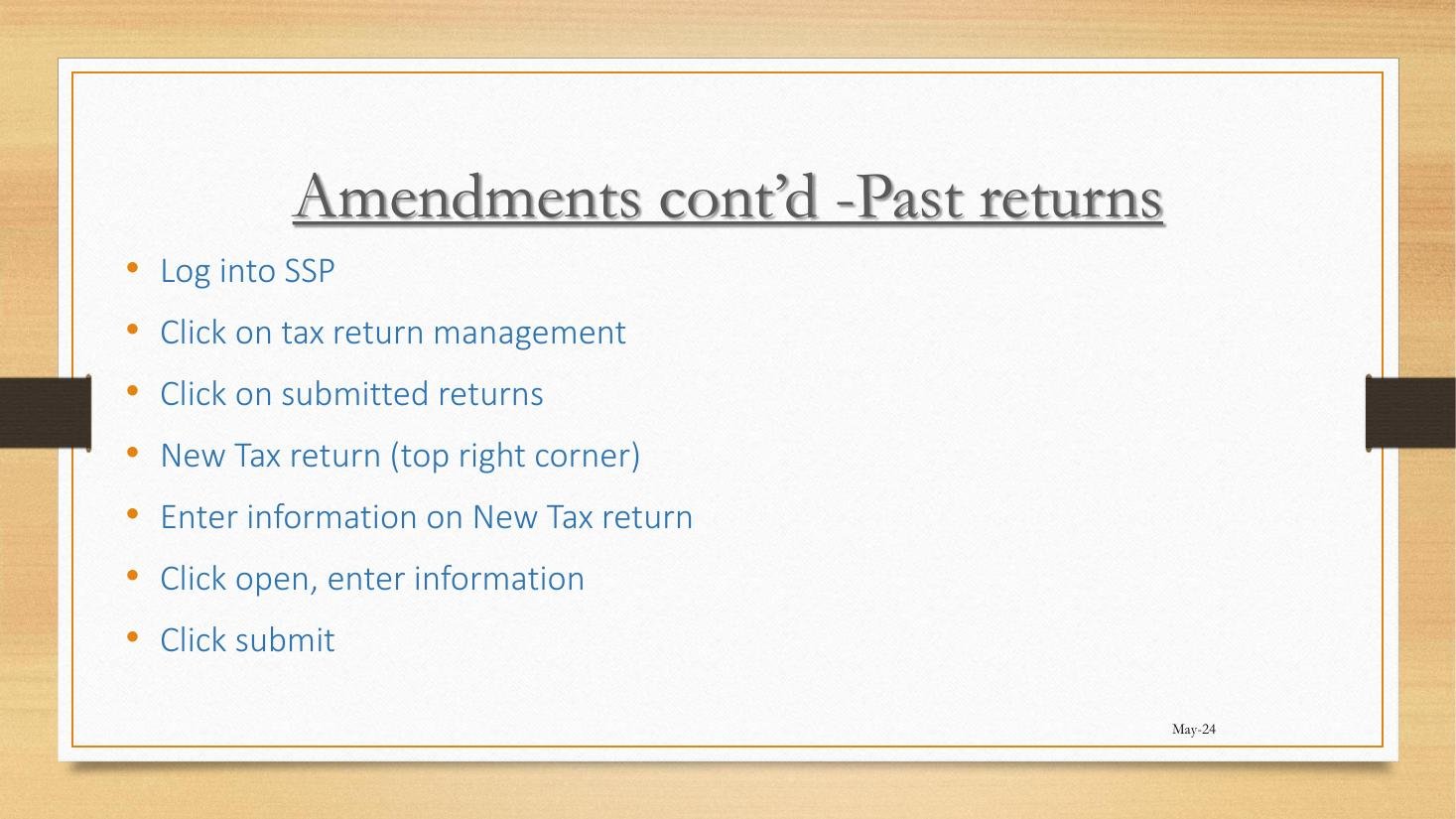

1. The seven-step workflow

- Login to SSP → Tax Return Management.

- Click Submitted Returns.

- Click New Tax Return at the top right.

- Select the tax type and the period.

- Click Open.

- Enter the data for the period.

- Click Submit.

2. The pre-2024 PAYE concession

Pre-January 2024 PAYE periods may be back-filed with a blank template (without altering headings) accompanied by aggregate figures. This is a transitional concession from the TaRMS migration; do not extend to current periods.

3. The Voluntary Disclosure overlay

For substantive back-filing (multiple periods, material liability), lodge a VDA01 alongside the back-filed returns. The VDA01 narrates the omission, the steps taken to remediate, and the expected liability. Penalty waiver is then formally engaged.

4. The back-filing checklist

- Identify all missing periods within the six-year window.

- Reconstruct the underlying records (payroll registers, sales registers).

- Compute liability for each period.

- Compute interest from each original due date.

- Lodge VDA01 narrating the omission (if material).

- Use New Tax Return for each missing period in chronological order.

- Pay liability via Single Account; specify allocation by period via RefNum.

- Confirm Tax Type Report reflects each back-filed period.

5. The chronological order rule

Back-file the oldest period first. This avoids cascade effects on subsequent periods (e.g., a corrected stock figure in March affects April’s opening stock).

6. Interest and penalty

Interest accrues from the original due date for each period. Penalty is at ZIMRA’s discretion. Voluntary disclosure typically waives penalty; non-disclosure leading to audit-driven discovery typically does not.

D. Real-World Applicability

1. The new client with gaps

An agent takes on a new client and discovers 8 months of missing PAYE returns and 3 missing VAT returns. Workflow: lodge VDA01 narrating the situation; back-file each missing period in chronological order; pay total liability with interest via Single Account.

2. The migration-era gap

A taxpayer’s August 2023 PAYE was lost during the e-Services to TaRMS migration. Use the pre-2024 concession: blank template, aggregate figures, covering note explaining the migration loss.

3. The presumptive-tax informal trader

An informal trader registered for Presumptive Tax in 2022 but never filed any quarterly returns. Lodge VDA01; back-file the eight quarterly returns; pay total liability.

4. The cleanup project plan

| Week | Activity |

|---|---|

| 1 | Diagnostic: identify all missing periods. |

| 2–3 | Reconstruct underlying records. |

| 4 | Compute liability + interest by period. |

| 5 | Lodge VDA01 with covering memorandum. |

| 6–7 | Back-file each period in chronological order. |

| 8 | Settle Single Account. |

| 9 | Reconcile Tax Type Report; confirm clean position. |

E. Case Law Integration

1. Voluntary Disclosure Cases — ZIMRA practice

Multiple unreported VDA01 cases settled in 2024 confirm the penalty-waiver pattern: full waiver where disclosure precedes audit; partial where disclosed during audit but before assessment.

2. Commissioner-General v. Hwange Trading (Special Court 2017)

An old case but instructive: a taxpayer who back-filed years 2009–2014 in 2017 was held to be within the section 47 six-year window for 2011 onwards but statute-barred for 2009 and 2010. The back-filing for the older years was treated as voluntary additional payment; ZIMRA could not raise corresponding additional assessments.

3. The Magna Engineering principle revisited

Section 34B RAA (Commissioner’s prescribed manner) applies equally to back-filing. The SSP New Tax Return workflow is the prescribed channel; paper substitutes are not.

F. Common Pitfalls

1. Filing without VDA01 for a material gap

Penalty mitigation is lost. Fix: always lodge VDA01 if the gap is material.

2. Filing in non-chronological order

Cascade errors. Fix: oldest first.

3. Forgetting interest

Interest from original due date on every back-filed period. Compute and pay.

4. Treating the six-year limit as absolute

Periods older than six years are statute-barred for assessment but the taxpayer may still volunteer payment if there is moral or commercial reason. Generally not advised.

5. Back-filing during audit

Coordinate with audit officer first. Unilateral back-filing during audit looks like manipulation.

6. Not reconstructing records adequately

A back-filed return that does not match the underlying records is worse than no return. Fix: reconstruct first, file second.

G. Knowledge Check

Question 1

What is the section 47 ITA reach-back window, and how does it constrain back-filing?

Question 2

What is VDA01 and when should it be lodged?

Question 3 — Scenario

A new client has 8 months of missing PAYE returns and 3 missing VAT returns. Sketch the cleanup project plan.

Question 4 — Scenario

A back-filing exercise reveals total liability of USD 18,000 plus interest of USD 1,400. The client cannot pay in one go. What are the options?

Question 5

What does Hwange Trading (2017) tell us about the statute-bar limit on back-filing?

H. Quiz Answers with Explanations

Answer 1

Section 47 ITA gives ZIMRA a six-year reach-back for additional assessments. Reciprocally, the practical back-filing window is six years — older periods are statute-barred for both ZIMRA assessment and meaningful back-filing.

Answer 2

VDA01 is the Voluntary Disclosure Application form. It should be lodged whenever a material gap is being remediated, before any audit selection. Penalty waiver is the typical outcome.

Answer 3

Per Section D4: weeks 1–9 covering diagnostic, record reconstruction, liability computation, VDA01 lodgement, chronological back-filing, Single Account settlement, and reconciliation.

Answer 4

Three options: (a) Lodge VDA01 with the back-filed returns; engage Debt Management module for a payment plan; ZIMRA can grant up to 12-month deferral on USD-denominated debt with interest. (b) Pay in full now using a bridging loan; the interest cost may be lower than ZIMRA’s prescribed rate. (c) Lodge an application for compounded payment terms direct to the Commissioner-General. Option (a) is most common.

Answer 5

Commissioner-General v. Hwange Trading (Special Court 2017) confirmed that periods older than the six-year window are statute-barred. Back-filing those older periods does not extend the section 47 reach-back; ZIMRA cannot raise additional assessments on years already statute-barred.

I. Key Takeaways

- Section 47 ITA — six-year reach-back, in both directions.

- Voluntary Disclosure (VDA01) is the penalty-waiver mechanism.

- Workflow: Submitted Returns → New Tax Return → choose period → submit.

- Chronological order: oldest first.

- Interest from original due date on every back-filed period.

- Pre-2024 PAYE concession: blank template + aggregate figures (transitional only).

- Do not back-file during audit without coordination with audit officer.

- Continuity: Module 5 next covers Tax Clearance Certificates — the document a clean back-filing exercise unlocks.