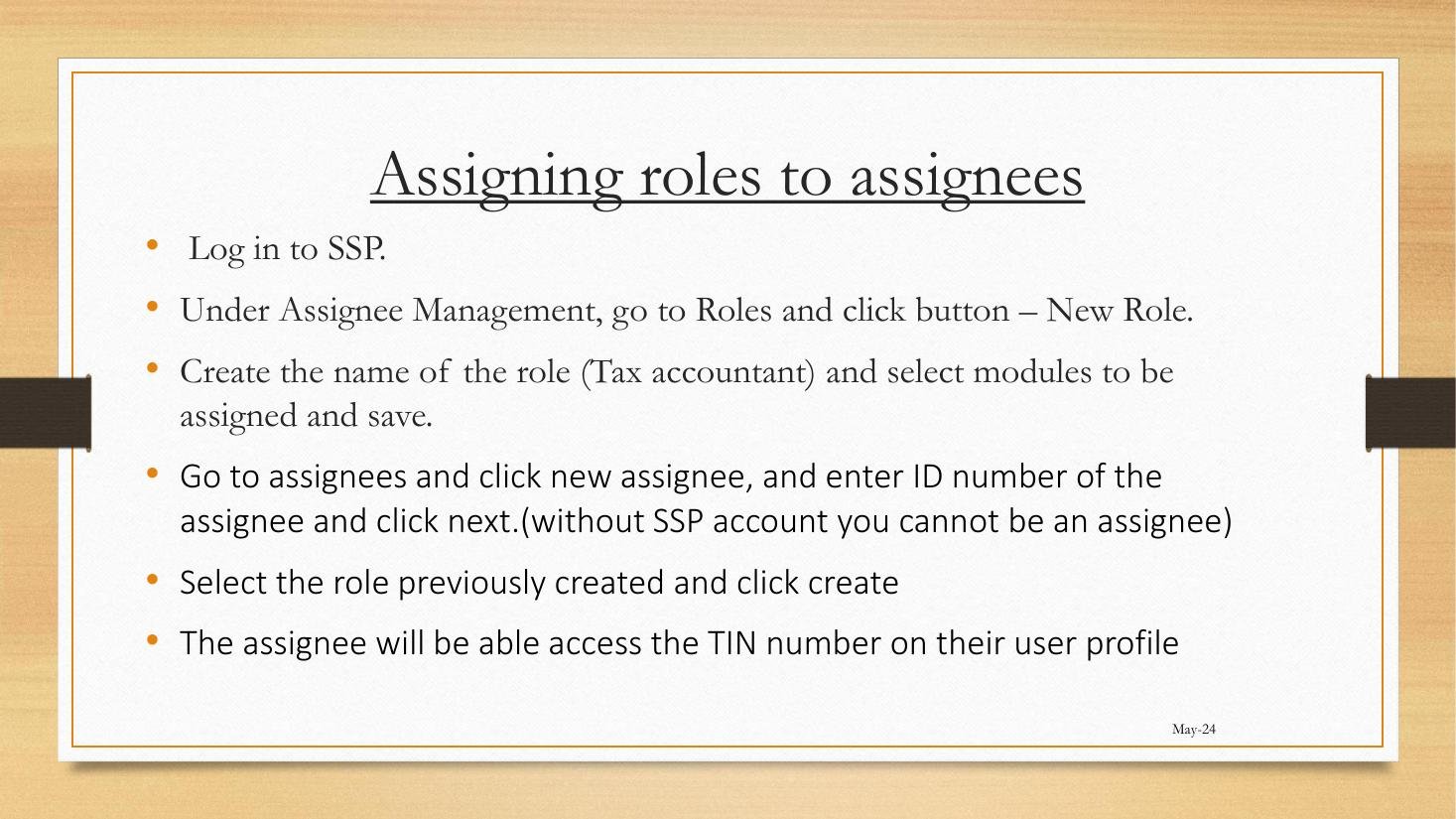

Lessons 3.1–3.3 dealt with the relationship between client and agent firm. Lesson 3.4 turns inward: how the firm structures itself within TaRMS so that an articled clerk can prepare returns, a manager can review them, and a director can submit, without any of the three using a shared password.

The same Roles-and-Assignees architecture applies to corporate finance teams — an in-house tax department of six people structures itself in exactly the same way. Module 3 is therefore not just for tax agents; it is for every organisation that has more than one person touching ZIMRA filings.