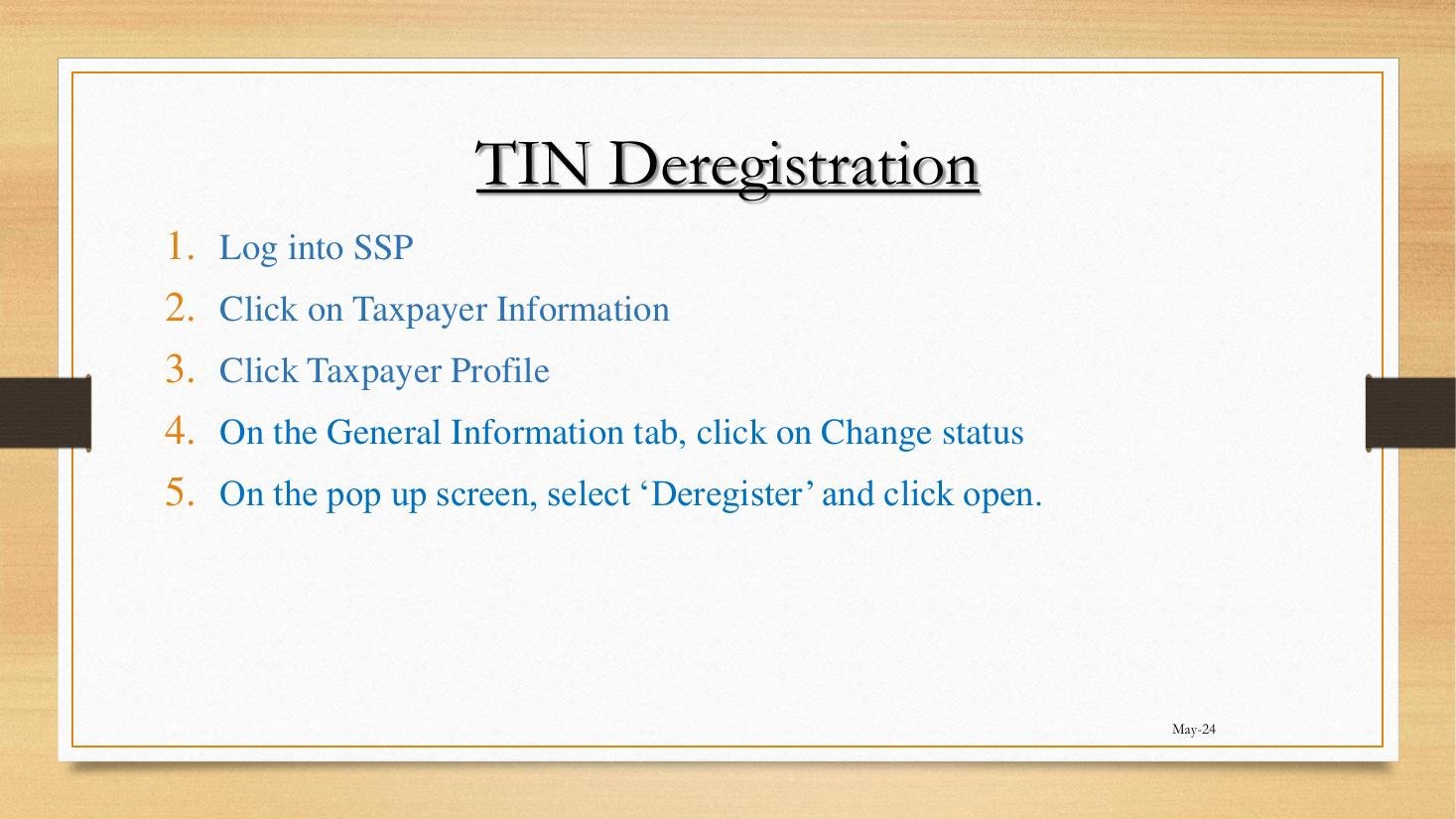

Module 2 began with adding tax types and ends with closing the whole record. TIN deregistration is the most consequential single action a taxpayer ever performs in TaRMS — it terminates the relationship with ZIMRA at the master-record level. It is rare, but when it happens, it must happen correctly.

Three predicates make TIN deregistration appropriate: cessation of trade with no expectation of resumption; death of an individual taxpayer (handled by the executor); and final dissolution of a company at the registrar of companies.